What is an ISA?

An ISA, short for Individual Savings Account, is a type of tax-efficient savings or investment account available to UK residents. If you are wondering what is an ISA in the UK, it essentially allows you to save or invest money without paying tax on the interest, dividends or capital gains earned, up to certain limits set by HMRC. This makes it a popular choice for building wealth over time, whether through safe cash savings or higher-risk investments.

Definition and full form

The full term for an ISA is Individual Savings Account, and what is an ISA account in the UK boils down to a wrapper around your savings or investments that shields them from UK income tax and capital gains tax. Unlike regular savings accounts, where interest might push you into a higher tax bracket, ISAs keep your returns tax-free. Introduced to promote long-term saving, they come in various forms to suit different financial goals, from emergency funds to retirement planning.

History and purpose

ISAs were launched in 1999 by the UK government to replace personal equity plans and TESSAs, aiming to encourage more people to save amid low savings rates. The purpose remains to help UK residents grow their money tax-efficiently, especially in an era of rising living costs. Over the years, the scheme has evolved, with updates like the Lifetime ISA in 2017 to support first-time buyers and retirement savers, as detailed in official GOV.UK guidance on how ISAs work.

Key benefits

The primary benefit of an ISA is tax-free growth: no income tax on interest from cash ISAs or dividends from investments, and no capital gains tax on profits from selling assets. This can significantly boost returns over time—for instance, a £10,000 investment growing at 5% annually would save you hundreds in taxes after a decade. ISAs also offer flexibility, with options for easy access or fixed terms, making them suitable for beginners starting their savings journey.

Types of ISAs available

Understanding the types of ISAs helps you choose one that fits your needs, whether you prefer low-risk cash savings or potential higher returns from investments. There are five main types, each with unique features for different life stages and goals.

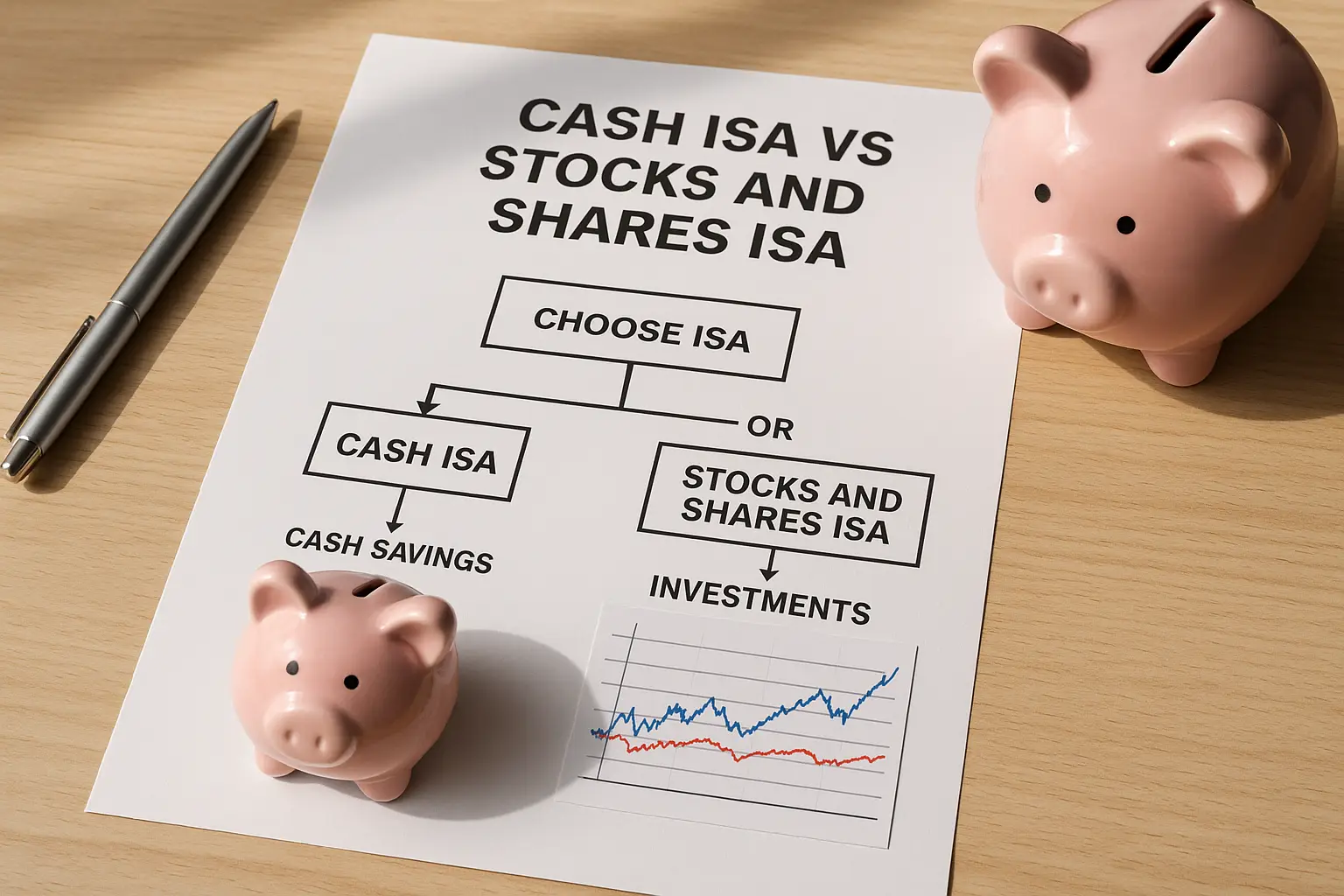

Cash ISA

A cash ISA is like a regular savings account but tax-free—what is a cash ISA in the UK? It holds cash and pays interest without tax deductions, ideal for short-term savings. Rates vary, but it’s low-risk with your money protected up to £85,000 by the Financial Services Compensation Scheme.

Stocks and shares ISA

This investment ISA, often called a stocks and shares ISA, lets you invest in shares, funds, bonds or ETFs within a tax-free wrapper. What is a stocks and shares ISA in the UK? It’s for those comfortable with market fluctuations, offering potential for higher returns than cash but with capital risk—your investment value can fall.

Lifetime ISA

A Lifetime ISA (LISA) is designed for 18- to 39-year-olds saving for a first home or retirement—what is a Lifetime ISA in the UK? You can contribute up to £4,000 annually and get a 25% government bonus, up to £1,000, as explained by MoneySavingExpert’s guide to ISA types. Withdrawals for non-qualifying reasons incur a 25% charge to recoup the bonus.

Junior ISA

A Junior ISA is for children under 18, set up by parents or guardians—what is a Junior ISA in the UK? It allows tax-free growth on savings or investments until the child turns 18, with an annual limit of £9,000 for 2024/25. Funds become accessible at 18, promoting early saving habits.

Innovative finance ISA

This type covers peer-to-peer loans and crowdfunding, offering tax-free returns on alternative investments. It’s suited for those seeking diversification beyond traditional stocks or cash, though it carries higher risks like lender defaults.

| Type | Key features | Risks | Suitability |

|---|---|---|---|

| Cash ISA | Tax-free interest; easy or fixed access | Low; inflation may erode value | Short-term savings, beginners |

| Stocks and shares ISA | Invest in markets; potential high growth | High; market volatility | Long-term investing, higher risk tolerance |

| Lifetime ISA | 25% bonus; home or retirement focus | Withdrawal penalties | First-time buyers aged 18-39 |

| Junior ISA | Tax-free for children; £9,000 limit | Locked until 18 | Parents saving for kids |

| Innovative finance ISA | P2P lending; alternative yields | Default risk | Diversified portfolios |

ISA allowance and rules

The ISA allowance sets how much you can contribute tax-free each tax year, which runs from 6 April to 5 April. For 2024/25, it’s £20,000—what is the ISA allowance in the UK? You can split this across types, but rules ensure compliance to maintain tax benefits.

Annual limit

With an ISA allowance of £20,000 for 2024/25, as per Barclays’ guide to ISAs, you can put this amount into ISAs combined. This limit resets each tax year, allowing fresh contributions—yes, you can put £20,000 in an ISA every year if eligible.

How many ISAs can you have

You can hold multiple ISAs but subscribe (add new money) to only one of each type per tax year—what is the rule on how many ISAs can I have? For example, one cash ISA and one stocks and shares ISA in a year, but you might keep older ones open.

Eligibility and subscriptions

UK residents aged 16+ for cash or 18+ for stocks and shares are eligible; non-residents generally cannot open new ISAs. Subscriptions count only new contributions, not transfers between your ISAs.

Tax year basics

The UK tax year starts 6 April, so plan contributions accordingly to maximise your allowance. Exceeding it voids the excess from tax protection.

How to open and manage an ISA

- Choose your type based on goals, like a cash ISA for safety.

- Compare providers via sites like MoneySavingExpert, ensuring FCA regulation.

- Apply online or in-branch with ID and address proof; declare it’s your one subscription per type.

- Fund via bank transfer; monitor via app or statements.

Transfers and withdrawals

Transfer ISAs between providers tax-free without using allowance. Withdrawals are flexible in easy-access types but may incur penalties in fixed ones.

Common mistakes to avoid

Avoid exceeding limits or forgetting the tax year end; always check eligibility first.

Tip for beginners: Start small with a cash ISA to build confidence before exploring investments. Track your contributions to stay within the £20,000 allowance, and review annually as rates change—see our best isa rates uk guide for options.

Benefits and tax advantages

ISAs shine in tax savings: no income tax on interest (up to £1,000 otherwise for basic-rate taxpayers) or capital gains tax (10-20% on profits outside ISAs), per Darlington Building Society’s ISA beginner guide.

Tax-free savings

All growth—interest, dividends, gains—is tax-free within limits, shielding savers from HMRC.

Comparison to regular accounts

Regular savings face tax; a £5,000 cash ISA at 4% yields £200 tax-free, versus £160 after 20% tax on a standard account.

Long-term planning tips

Use ISAs for goals like retirement; diversify types for balanced risk.

Frequently asked questions

What is the ISA allowance for 2024/25?

The ISA allowance for 2024/25 is £20,000, allowing UK residents to contribute this amount across all ISA types tax-free. This limit applies per tax year, from 6 April 2024 to 5 April 2025, and resets annually. It’s designed to encourage saving, but exceeding it means the excess isn’t protected—always track contributions to avoid penalties.

How does a cash ISA work?

A cash ISA works by letting you deposit money into a tax-free savings account where interest accrues without income tax deductions. You can choose easy-access for flexibility or fixed-rate for higher yields with lock-ins. Protected up to £85,000, it’s ideal for emergency funds, though returns may not beat inflation.

Can I have more than one ISA?

Yes, you can have multiple ISAs, but you can only subscribe new money to one of each type per tax year—for instance, one cash and one stocks and shares. Holding old ISAs open is fine, and transfers don’t count as subscriptions. This rule, from GOV.UK, allows diversification without losing tax benefits.

What is a stocks and shares ISA?

A stocks and shares ISA is an investment account for buying shares, funds, or bonds tax-free on gains and dividends. Unlike cash ISAs, it involves market risk, so value can fluctuate. Suited for long-term growth, it offers higher potential returns; beginners should start with low-cost index funds.

Who is eligible for a Lifetime ISA?

Eligibility for a Lifetime ISA includes UK residents aged 18 to 39 who haven’t owned a home before, using it for first-home deposits under £450,000 or retirement from age 60. You can contribute up to £4,000 yearly for a 25% bonus. Non-qualifying withdrawals face a 25% charge; it’s a powerful tool for young savers planning major life goals.

What happens if I exceed the ISA limit?

If you exceed the ISA limit, the excess contributions lose tax protection and may be taxed as regular income or gains. HMRC can void the entire ISA if rules are breached severely, though usually just the overage is affected. To avoid this, monitor your £20,000 allowance closely and consult providers before adding funds.

Can non-UK residents open an ISA?

Non-UK residents generally cannot open new ISAs, though they can manage existing ones until maturity. Eligibility requires UK residency during the tax year of subscription; expats should check GOV.UK’s ISA opening rules. Returning residents can reopen once eligible, preserving past tax benefits.