What is a Junior ISA and who is eligible?

A Junior ISA, often abbreviated as JISA, is a tax-free savings or investment account designed for children under 18 in the UK. It allows parents, guardians, or other responsible adults to save or invest on behalf of a child, with the funds growing free from income tax and capital gains tax until the child turns 18. This makes it an excellent way to build a financial nest egg for your child’s future, such as for education or a first home.

Definition and benefits

Introduced in 2011 as a replacement for Child Trust Funds, a Junior ISA helps secure your child’s financial future by offering tax-efficient growth. The key benefit is that any interest earned on cash savings or gains from investments are not taxed, unlike regular savings accounts where even small amounts of interest could be taxable for higher-rate taxpayers. According to MoneySavingExpert, this tax-free status can significantly boost long-term savings compared to standard child savings accounts.

Age and residency requirements

To open a Junior ISA, the child must be under 18 years old and a UK resident. There is no minimum age, so you can start saving from birth. The child cannot open the account themselves; it must be done by a parent or legal guardian, as outlined by GOV.UK guidelines.

Parental responsibilities

As the parent or guardian, you manage the account until the child reaches 18, when control passes to them. You are responsible for making contributions within the annual limits and choosing suitable investments if opting for a stocks and shares version. Remember, only one Junior ISA per child is allowed at a time, either cash or stocks and shares.

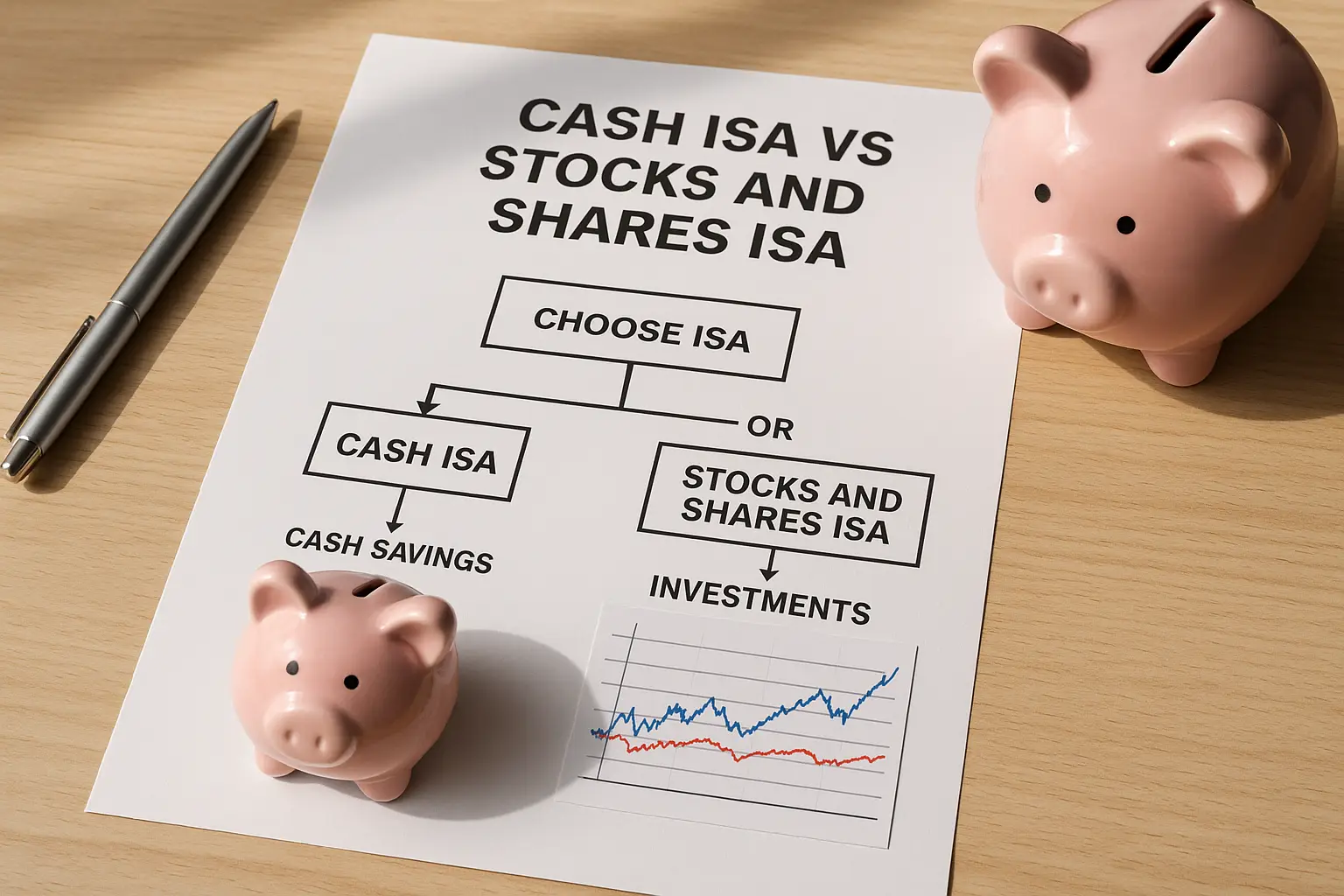

Types of Junior ISAs: Cash vs stocks and shares

Junior ISAs come in two main types: cash and stocks and shares, each suited to different risk levels and goals. Understanding the differences helps when deciding how to open a Junior ISA account that aligns with your family’s financial plans.

Cash ISA overview

A Junior Cash ISA works like a savings account, where money earns interest at a fixed or variable rate. It’s low-risk, with your capital protected, making it ideal for cautious savers. Providers like NS&I offer rates around 4% for 2025, backed by the government for security.

Stocks and shares ISA overview

A Junior Stocks and Shares ISA invests in funds, shares, or bonds, potentially offering higher returns but with market risks. The value can go down as well as up, so it’s better for those comfortable with volatility over the long term, like 18 years until access.

Choosing the right type

Consider your risk tolerance: opt for cash if you prioritise safety, or stocks and shares for growth potential. Many parents start with cash and switch later. For more on comparisons, see our guide on what is a junior isa.

| Type | Risk Level | Potential Returns | Minimum Deposit | Example Providers |

|---|---|---|---|---|

| Cash ISA | Low | Interest-based (e.g., 4% AER) | £1 or none | NS&I, Nationwide |

| Stocks and Shares ISA | Medium to High | Market-dependent (historical avg. 5-7%) | £100 or none | Hargreaves Lansdown, Trading 212 |

Step-by-step guide to opening a Junior ISA

Opening a Junior ISA is straightforward and can often be done online in minutes. Follow these steps to get started for 2025.

Gather required documents

You’ll need the child’s full name, date of birth, address, and your own ID as the applicant (e.g., passport or driving licence). If the child has a National Insurance number, have it ready, though it’s not always mandatory for under-16s.

Choose a provider

Research banks, building societies, or investment platforms authorised by the Financial Conduct Authority (FCA). Compare fees, rates, and ease of use. For investment options, platforms like Hargreaves Lansdown provide diverse choices.

Apply online or in-branch

Most providers allow you to open a Junior ISA online, which is quickest. Fill in the application form with child and applicant details, declare eligibility, and sign electronically. In-branch applications suit those preferring face-to-face help, like at Halifax.

Fund the account

Transfer money via bank transfer, debit card, or cheque. Start with as little as £1 for many accounts. Set up standing orders for regular contributions to maximise the £9,000 annual allowance.

Common timelines and tips

Applications typically process in 5-10 working days, faster online. Tip: Double-check eligibility to avoid rejection.

Minimum requirements and allowance limits for 2025

Understanding limits ensures you comply with HMRC rules when learning how to open a Junior ISA for your child.

Deposit minimums

Most providers require no minimum to open, with £1 being common for initial deposits. For example, NS&I’s Junior ISA starts at £1, as per their 2025 details.

Annual contribution cap

The Junior ISA allowance for the 2025/26 tax year (6 April 2025 to 5 April 2026) is £9,000 total across all JISAs. Unused allowance doesn’t carry over.

Transferring from Child Trust Fund

If your child has a Child Trust Fund, you can transfer it tax-free to a JISA. Contact the current provider and new one; the process takes up to 15 days. GOV.UK provides full guidance on how to open a Junior ISA UK with transfers.

Popular providers and how to open with them

Several trusted providers offer Junior ISAs. Here’s a brief on opening with key ones, without endorsement.

Hargreaves Lansdown process

Hargreaves Lansdown excels in stocks and shares. Apply online via their site, providing ID and child details. Funding starts immediately post-approval.

Nationwide and Halifax specifics

For Nationwide, open a Junior Cash ISA online or in-branch; they require child’s birth certificate. Halifax offers similar, with quick online setup for existing customers. Both suit cash savings.

Trading 212 for investments

Trading 212 is app-based for easy stocks and shares access. Download the app, verify identity, and fund via card. Ideal for tech-savvy parents.

For broader options and rates, check our pillar on the best junior isa. If considering long-term planning, explore junior isa vs junior pension.

Frequently asked questions

How old does a child need to be to open a Junior ISA?

There is no minimum age; you can open a Junior ISA from birth up to the child’s 17th birthday. This allows early saving for newborns, with parents managing until 18. As per GOV.UK, eligibility hinges on UK residency, making it accessible for infants whose families want tax-free growth from day one.

How long does it take to open a Junior ISA?

Online applications often approve within 24-48 hours, with full setup in 5-10 days including verification. In-branch can be instant but may take longer for processing. Factors like document checks affect timelines, so prepare in advance for smoother how to open a Junior ISA account online experiences.

Can I open a Junior ISA for my grandchild?

Yes, grandparents can open and manage a Junior ISA if they have parental responsibility or the parents consent. It’s a great gifting option within the £9,000 allowance. Consult GOV.UK for legal responsibilities to ensure compliance and avoid disputes.

What is the minimum amount to open a Junior ISA?

Many providers, like NS&I, allow opening with just £1 or even no initial deposit. This low barrier encourages starting small. Always check the specific provider’s terms, as some investment platforms may require £100 for stocks and shares to cover fees effectively.

What happens to a Junior ISA at 18?

At 18, the account matures, and the child gains full control; it converts to an adult ISA with a £20,000 allowance. Parents lose management rights, so discuss plans early. If untouched, it remains tax-free, but withdrawals before 18 incur penalties.

How do I transfer a Child Trust Fund to a Junior ISA?

Contact both the CTF provider and your chosen JISA provider to initiate a free transfer. It must be done directly to stay tax-free, taking 10-15 days. This upgrade often yields better returns; MoneySavingExpert advises comparing rates first for optimal growth strategies.

Opening a Junior ISA is a smart step towards your child’s financial security. With tax-free benefits and flexible options, start today by choosing a provider and applying online. For personalised advice, consult a financial adviser.