Lifetime ISA withdrawal rules and penalties: Avoid costly mistakes

The lifetime ISA withdrawal penalty is a 25% charge imposed by HMRC, the UK’s tax authority, on non-permitted withdrawals from your Lifetime ISA (LISA), effectively wiping out the government bonus and more. This penalty applies unless you’re buying your first home under £450,000 or have reached age 60, helping savers avoid unexpected losses amid rising housing costs. In this guide, we’ll break down the rules, calculations, and strategies to protect your savings, drawing on official 2025 updates.

Understanding Lifetime ISA withdrawal penalties

The core rule for lifetime ISA withdrawal penalties in the UK is straightforward: any money taken out before qualifying conditions are met triggers a 25% government charge on the full amount withdrawn, not just the bonus. This discourages early access and ensures the scheme supports long-term goals like homeownership or retirement. Launched in 2017, the LISA offers a 25% bonus on contributions up to £4,000 annually, but strict rules govern access to maintain its tax-free status.

What triggers the 25% penalty

A lifetime ISA penalty withdrawal occurs if you access funds for anything other than permitted uses, such as emergencies, non-first-home purchases, or before the account’s one-year anniversary. Early withdrawal penalties apply even to small amounts, with HMRC recovering the bonus plus an extra 6.25% from your own savings. For instance, withdrawing during financial hardship without eligibility leads to immediate deduction, as outlined on GOV.UK (accessed 2025).

How the penalty is calculated

The lifetime ISA withdrawal penalty calculation is simple: multiply your total withdrawal (contributions + bonus + growth) by 25%, then subtract that from the amount. This recovers the government’s 25% bonus entirely and penalises 6.25% of your contributions. Use this step-by-step guide: 1) Identify total balance withdrawn; 2) Apply 25% charge; 3) Receive net amount after deduction, often handled automatically by your provider.

Impact on bonus and contributions

The penalty hits the entire pot, meaning you lose the full government bonus—worth up to £1,000 yearly—and part of your savings. If your LISA has £4,000 in contributions plus £1,000 bonus, withdrawing £5,000 incurs a £1,250 charge, leaving you with £3,750, a net loss beyond the bonus. This structure, per Tembo (updated 2025), underscores why planning is crucial for first-time buyers eyeing the £450,000 house limit.

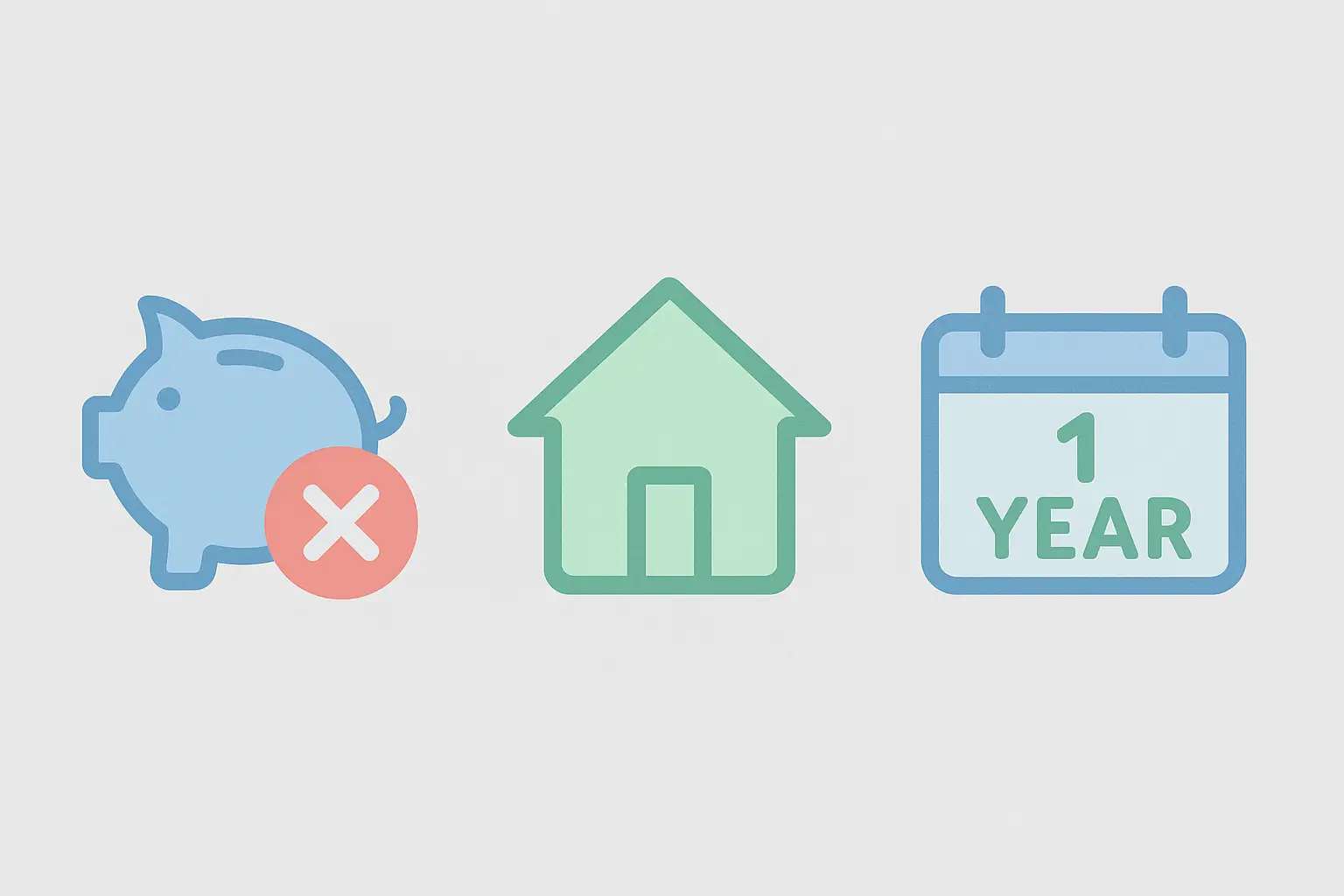

Permitted withdrawals without penalty

You can withdraw from a Lifetime ISA tax-free for buying your first home up to £450,000 after one year, reaching age 60 for retirement, or in cases of terminal illness, avoiding the 25% hit entirely. These exceptions preserve your savings and bonus, aligning with the scheme’s goals. Always confirm eligibility with your provider to ensure compliance under 2025 rules.

First-time home purchase rules

For first-time buyers, lifetime ISA withdrawal rules allow penalty-free access if the property costs £450,000 or less and the account is at least one year old. You can use up to the full balance, including bonus, towards the deposit. This benefit, detailed on AJ Bell, supports over 129,000 savers annually but requires conveyancer notification.

Retirement access at age 60

At age 60, you can withdraw the entire LISA tax-free for any purpose, including retirement income, with no lifetime ISA penalty withdrawal charge. Growth and bonus remain yours, making it a flexible pension alternative. Note that contributions stop at 50, per official guidelines.

Terminal illness exceptions

If terminally ill (life expectancy under 12 months), you can access funds without penalty, certified by a doctor. This compassionate rule ensures funds for care without financial loss. Providers like Skipton explain this in their withdrawal charges guide.

Avoiding costly withdrawal mistakes

To dodge the lifetime ISA early withdrawal penalty, plan around permitted uses and consider transfers to other ISAs, preserving your tax-free growth without charges. With 2025 seeing penalties rise 35%, proactive steps like building an emergency fund outside the LISA are essential. Linking to what is a lifetime isa can help clarify basics before committing.

Planning for eligible use

Align your LISA with home-buying timelines: save for at least a year and target properties under £450,000 to withdraw penalty-free. Use tools to track eligibility and combine with schemes like Help to Buy. For deeper insights, see lifetime isa rules and regulations.

Transfer options to other ISAs

Transferring to a stocks and shares ISA or cash ISA avoids penalties, keeping your money tax-free but losing the LISA bonus—notify HMRC within limits. This suits changing needs without full withdrawal. Providers handle this seamlessly.

Recent 2025 rule updates

No major changes to the 25% lifetime ISA withdrawal penalty in 2025, but rising house prices push more towards penalties; reforms are discussed but unchanged per GOV.UK. Stay informed via official updates to adapt strategies.

Quick tips to avoid penalties:

- Hold for one year minimum.

- Verify first-time buyer status.

- Build separate emergency savings.

- Consult providers like Moneybox for the Moneybox lifetime ISA withdrawal penalty specifics.

Lifetime ISA penalty calculator and examples

A lifetime ISA withdrawal penalty calculator reveals the true cost: for every £1 withdrawn, expect to lose £0.25 to HMRC. Real scenarios show varying impacts based on balance; providers may vary slightly in processing. This section provides a simple tool and examples to forecast losses.

Step-by-step calculation guide

To use a lifetime ISA penalty withdrawal calculator: total your pot (e.g., £10,000), subtract 25% (£2,500), receive £7,500. Factor in growth for accuracy. Online tools from providers aid this.

Real-world scenarios

Scenario: £4,000 contributed + £1,000 bonus = £5,000 withdrawn; penalty £1,250, net £3,750 (lose all bonus + £250 own money). Another: £1,000 + £250 bonus = £1,250 withdrawn; net £937.50. These highlight risks for young savers.

| Contributions | Bonus (25%) | Total Withdrawn | Penalty (25%) | Net Received |

|---|---|---|---|---|

| £1,000 | £250 | £1,250 | £312.50 | £937.50 |

| £2,000 | £500 | £2,500 | £625 | £1,875 |

| £4,000 | £1,000 | £5,000 | £1,250 | £3,750 |

Provider-specific variations

While the 25% rate is uniform, providers like Moneybox process deductions instantly; check terms. For the best lifetime isa options, compare fees alongside penalty rules.

Latest statistics and reforms

In 2024/25, lifetime ISA withdrawal penalties hit £102 million, up 35% from £75.5 million, affecting 129,000 savers amid housing woes. Calls for reform grow, with 42% favouring penalty-free access to own contributions. These trends, from The Independent (2025), signal potential 2026 changes.

2024/25 penalty trends

Penalties soared due to delayed home buys, with nearly 100,000 hit last year per GB News. This 35% rise fuels debates on scheme equity for under-40s.

Government calls for change

HMRC surveys show 42% support reforming to allow own-savings withdrawal without loss, despite £3bn cost fears by 2041 (MoneySavingExpert, 2025). No 2025 alterations yet, but monitor budgets.

Frequently asked questions

Can I withdraw from a Lifetime ISA without penalty?

Yes, you can withdraw penalty-free from a Lifetime ISA for specific reasons like buying your first home up to £450,000 after one year or at age 60 for retirement. Terminal illness also qualifies, allowing full access without the 25% charge. These rules, set by HMRC, ensure the scheme benefits long-term savers while protecting against misuse.

What is the Lifetime ISA withdrawal charge?

The Lifetime ISA withdrawal charge is a flat 25% penalty on the entire amount withdrawn if not for permitted uses, recovering the government bonus and penalising contributions. This applies UK-wide under 2025 regulations, processed by your provider. It’s designed to enforce the scheme’s focus on homeownership and retirement, avoiding early dips into tax-free savings.

How much is the Lifetime ISA penalty?

The Lifetime ISA penalty is 25% of your total withdrawal, equating to full bonus recovery plus 6.25% of your input. For a £5,000 pot, that’s £1,250 deducted, leaving £3,750. This structure, unchanged in 2025 per GOV.UK, impacts thousands annually and highlights the need for strategic saving.

When can I withdraw from Lifetime ISA tax-free?

You can withdraw tax-free from a Lifetime ISA after one year for a first home ≤£450,000, at age 60 anytime, or if terminally ill. These are the only exemptions from the withdrawal penalty, preserving bonus and growth. For first-time buyers, timely planning maximises this benefit amid rising UK property prices.

Does the Lifetime ISA penalty apply to the bonus only?

No, the Lifetime ISA penalty applies to the full withdrawal amount, not just the bonus, resulting in a net loss on your contributions too. This 25% charge ensures the government’s incentive isn’t abused for short-term needs. As per official rules, it affects the whole pot, making alternatives like regular ISAs better for flexible access.

Is the lifetime ISA withdrawal penalty changing in 2025 UK?

The lifetime ISA withdrawal penalty remains 25% in 2025 UK, with no confirmed changes despite reform calls from rising penalty totals of £102m. HMRC surveys indicate potential future tweaks, like sparing own savings, but current rules hold firm. Savers should track budget announcements for updates that could ease first-time buyer burdens.

What is the lifetime ISA early withdrawal penalty for emergencies?

The lifetime ISA early withdrawal penalty for emergencies is the standard 25% charge, as non-permitted access doesn’t qualify for exceptions. This can leave you worse off, losing bonus and part of contributions during tough times. Experts recommend separate emergency funds to sidestep this, aligning with broader ISA strategies for financial resilience.